Among dozens of investing books I have read so far, “The Ultimate Dividend Playbook” by Josh Peters is the best one for dividend growth investing.

Recently I just re-read it. There are many details in the book that I understand deeper and resonate more now. Here are some important topics and my (confirming or different) comments.

Three Portfolios to Live Off Retirement

The book mentions three type of portfolios to provide income during retirement. Basically you retrieve some money from portfolio in some way annually, and traditional wisdom is that you can withdraw 4% of the portfolio value without draining your portfolio in the long run.

- Investing in stock market index, e.g. S&P500. The index currently is providing less than 2% of dividends as income, so you need to sell some holdings annually to keep the 4% withdrawal rate. The portfolio value is volatile – sometimes you sell fewer shares when the market is up-trending and sometimes you sell more shares when the market i in downturn. Timing is important but you can’t control that.

- Investing in bonds. The coupons paid by bonds don’t change and the portfolio value is less volatile over the time. However the portfolio value is highly sensitive to interest rates and the coupons don’t grow with inflation. You need to reinvest part of the income back to portfolio for future income to grow.

- Focus on dividend growth investing. You can configure so that the target yield of the portfolio is around 4% and you don’t need to sell any positions to cover living expense. When done right the positions will grow as prices appreciate together with bigger dividends year of year.

My Comments: Obviously the third portfolio focusing on dividend growth stocks with both income and growth components is the best for retirement. Dividend growth investing is not a new concept but recently gaining more traction among Millennial and Gen-Z investors.

Gordon Growth Model

The book mentions Gordon Growth Model, which relates the expected return of a dividend growth stock to the growth rate and its yield:

Dividend Yield + Dividend Growth = Prospective ReturnMy Comments: This formula is originally transformed from Gordon Growth Model for mature stocks increasing dividends at a constant pace. But in fact it is applicable for any dividend paying stocks with any dividend growth rate and stability. It is an astounding connection that the return of the stock is just yield plus the dividend growth rate.

Realistic View of Market Condition

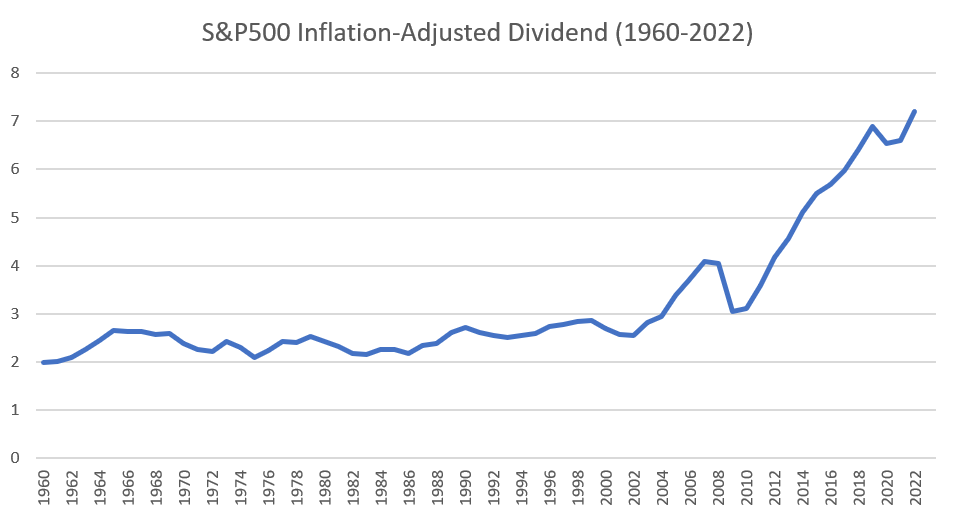

One thing I really like about the book, is that it doesn’t paint an overly glorious picture of dividend investing. From 1947 to 2006 (when the book was written), the dividend amount of S&P500 increased from $0.68 per share to over $25 per share. That was a very nice 6.2% annually. However, the book states that the real dividend growth after inflation is much less compelling. The average of inflation from 1947 to 2006 was 3.8%, leaving the real dividend growth after inflation at 2.4%.

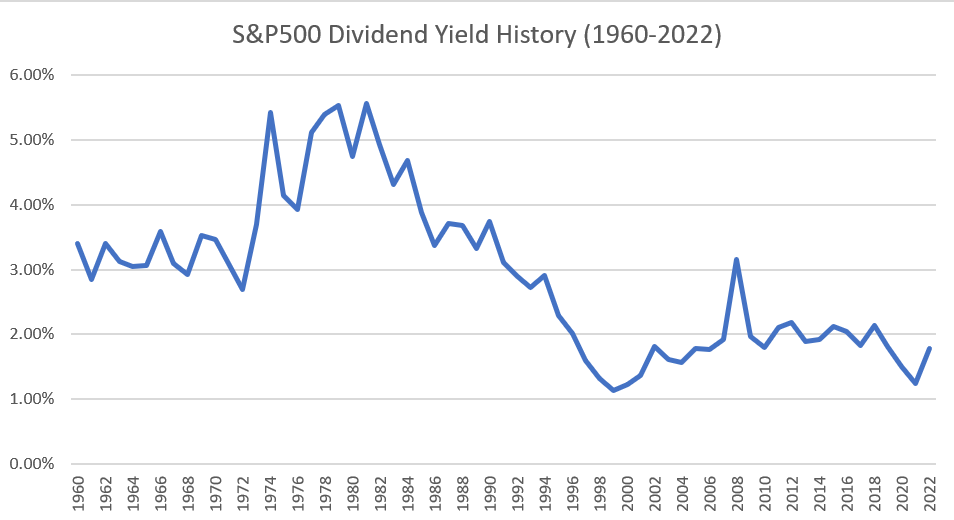

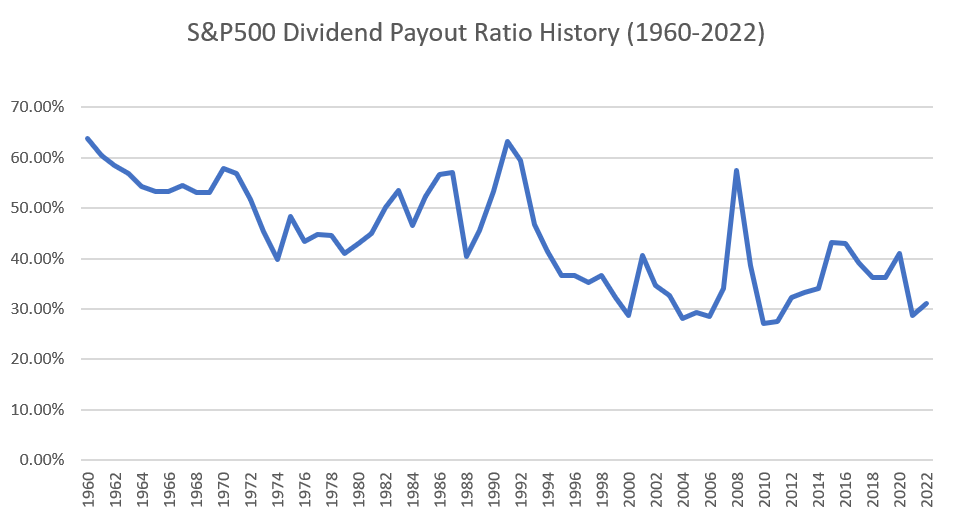

My Comments: I am very curious about what the market condition looks like today for dividend investing, so I found this data – many thanks to the diligent work of Professor Aswath Damodaran, the famous valuation guru. I extend the data from 2006 to 2022 and here are what they look like now:

The inflation from 1960-2022 was about 3.7% annually. Dividend growth from the same period was 5.9% so real dividend growth after inflation was 2.2%. In 2023 the inflation is pretty high at around 6% and could potentially stuck with 3-4%. The expected nominal dividend growth may be around 5-6%, plus the 1.8% yield, that’s about 7-8% return annually. The book also mentions that given payout ratio is at historical low, companies have been using the reserved cash to buy back shares, which may boost the dividend growth 1-2% higher. All in all we are expecting nominal total return from dividend growth investing around 8-10% for the overall market.

DDRM Explained

The book also describes a framework to analyze different types of dividend stocks. The author named it DDRM (Dividend Drill Return Model). While the name is not easy to remember, it is simple enough to answer three straightforward but important questions:

- Is this dividend safe?

- Will this dividend grow?

- What does this dividend stream stand to return to me as a shareholder?

My Comments: I do not intent to get into the details here because there are lot of mathematical details, but I started to use simple models like DDRM and one useful rating methodology from Dividend Scorecard to quantify the quality of dividend stocks before drill down into more details like durable economic moat, management quality, long term demands, etc.

Simple model is a double-edged sword. The downside of DDRM is it’s overly simplified to focus on total growth only. A lot of other topics discussed in the book like earning stability, earning durability, margin of safety, and yield history, etc. do not get quantified in the DDRM. For an experienced investor like the author, he likely knows what else to check and make qualitative decision but for a regular individual investor, it is better to have a model that factor in more risks and build more margin of safety, which we will talk about in the next section. On that front Dividend Scorecard has been doing well in terms of quantifying more factors into its rating system.

Margin of Safety

The book derives the margin of safety in dividend growth investing from its DDRM and contrasts that with typical margin of safety defined by broader stock investing. The typical stock investment risks are never about volatility for individual investors, it is always about the possibility of permanently loss of principals. For dividend investing, the required return defines the margin of safety, i.e. if you always look for stocks that are capable of reaching 12% return with dividend yield plus growth, that 1-2% extra requirement over market average return (8-10%) will help you a long way when things aren’t going the way you expected.

My comments: I resonate that the traditional risk definition by institutional investors – the volatility of stock price – is completely useless for individual investors. DDRM requires a few manual inputs so the return estimation is prone to human errors. However regardless of the estimation margin of errors, setting a higher bar for the expected returns can definitely reduce risks.

Yield History

Before hitting the “Buy” button after you perform a lot of checks for a single stock, it is wise to check its past yield history. If the current yield is too low by its historical standards, you’d better ask questions:

- Have dividend growth prospects changed materially for the better?

- Were past yields clearly too high for subsequent dividend growth potential?

On the other hand, if the current yield is too high compared to historical range, ask two opposite questions:

- Has the dividend become unsafe?

- Is dividend growth over?

My Comments: I rarely buy any stocks whose yield is in the lower end of past 5 years yield range or just enter the period of lowest yield in its history. Usually that is a very flourish period with a lot of growth in revenue, earnings, may be cash flows as well. A typical example in nowadays’ market is Microsoft. Before Microsoft’s cloud business entered into picture, the stock had yield over 2%. Then the yield has been always hanging around 1-2% since its cloud business took off. I am not saying Microsoft is not a good stock to own if the price is correct, but it is obvious that people are buying it for its growth and to a much less extent for its dividend. You need to be mentally prepared if one day the growth is going away, the price will get crashed.

Manage a Dividend Stocks Portfolio

The book provides some reasonable target yield for a dividend stocks portfolio. A 4% target yield is best for providing both income and growth. You can mix in a few high growth yield stocks while keeping some low growth but 5-6% yields to balance out. There are also some guidelines on when to sell a dividend stock. If the dividend becomes unsafe or you can absolutely improve yield or growth by swapping stocks.

My Comments: My personal ideal portfolio should have slightly over 3% as target yield. In that case I can mix in a lot of growth stocks paying and increasing dividends at 10-20% annually. For any investors still at working ages, focusing on growth while having some dividends to stabilize the portfolio volatility is a good trade-off. There are three scenarios to sell a stock in general stock investing. They are also applicable in dividend stocks context as well.

Rules to sell a (dividend) stock:

- Sell when the fundamentals of the stock deteriorates. In dividend growth investing context, that’s when the dividend become unsafe. The dividend is no longer covered by earnings or cash flows in the long run.

- Sell when the share price is overvalued. Luckily in dividend growth investing context, we can use yield + dividend growth rate as proxy for future returns. Many premium dividend paying stocks like O, KO are becoming too well known. Their future returns have fallen to 5-6%. They are not really worth owning for growth investors. You can just invest in index with 8-10% total return.

- Sell when there are better opportunities else where. In dividend growth investing context, if you find alternative stock that can provide same growth but better yield or same yield but better growth, go for it.

Disclaimer: The information contained on this site is provided with author’s personal opinions and is not for recommendations or solicitations of investments. Readers should consult professional advisors for more complete and current information to make investment decisions.